Mortgage insurance can feel like a financial weight for many homeowners. Understanding when mortgage insurance goes away is crucial for planning your finances, reducing monthly payments, and building home equity faster. In this comprehensive guide, we’ll explore the ins and outs of mortgage insurance, explain the rules that dictate when it ends, and offer tips for homeowners looking to eliminate it.

What Is Mortgage Insurance and Why Do You Pay It?

Mortgage insurance protects lenders, not borrowers. It’s required when a homebuyer makes a down payment of less than 20% of the property’s purchase price. Essentially, the lender is taking on more risk, so mortgage insurance mitigates that risk in case the borrower defaults.

There are two common types of mortgage insurance:

| Type | Applies To | Payment Method | Key Notes |

|---|---|---|---|

| Private Mortgage Insurance (PMI) | Conventional loans | Monthly premium added to mortgage | Can be canceled once equity reaches 20–22% |

| Mortgage Insurance Premium (MIP) | FHA loans | Upfront and/or monthly | May last the life of the loan unless refinanced |

For most homeowners, knowing when mortgage insurance goes away is a key part of financial planning.

When Mortgage Insurance Goes Away for Conventional Loans

For conventional loans with PMI, the rules for cancellation are clear:

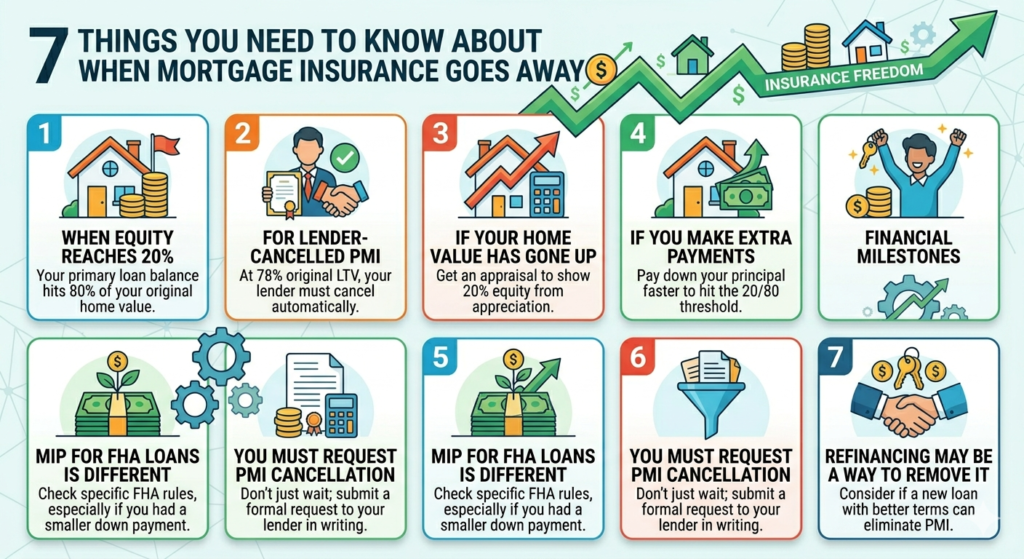

- Automatic Termination – Lenders are required by law (Homeowners Protection Act) to cancel PMI automatically when your loan balance reaches 78% of the original home value.

- Borrower Request – You can request PMI cancellation when your loan balance hits 80% of the original home value, provided you are current on payments.

For example, if you purchased a home for $300,000 with a 10% down payment ($30,000), your initial loan is $270,000. PMI can be canceled once your balance falls to $240,000 (80%) if you request it, and must be terminated at $234,000 (78%).

Tip: Keep an eye on your home’s value. If your home appreciates, you may reach the 80% threshold sooner. A new appraisal can help justify early cancellation.

When Mortgage Insurance Goes Away for FHA Loans

FHA loans work differently. Mortgage insurance premiums (MIP) are often required for either 11 years or the life of the loan, depending on your down payment.

| Down Payment | MIP Duration |

|---|---|

| ≥ 10% | 11 years |

| < 10% | Life of loan |

So, if you put less than 10% down, mortgage insurance stays until the loan is fully paid or refinanced. This distinction is critical because FHA MIP is non-negotiable unless you refinance into a conventional loan with sufficient equity.

Factors That Affect When Mortgage Insurance Goes Away

Several factors influence when mortgage insurance goes away:

- Original Loan Balance – Larger loans may take longer to reach the equity thresholds for cancellation.

- Property Appreciation – Rising home values can accelerate PMI removal.

- Extra Payments – Paying extra principal can help you reach 20% equity faster.

- Loan Type – FHA vs. conventional loans differ significantly in cancellation rules.

- Loan Age – Some lenders enforce a minimum period before PMI cancellation requests can be made (usually two years).

By actively managing these factors, homeowners can reduce the total cost of mortgage insurance.

How to Strategically Remove Mortgage Insurance Early

If you want to cut mortgage insurance costs sooner, consider the following strategies:

1. Make Extra Principal Payments

Even a small additional payment each month can bring your equity up faster, helping you reach the 20% threshold.

2. Request an Appraisal

If your home value has increased significantly, a professional appraisal can support PMI removal even if you haven’t paid down to 80% of the original balance.

3. Refinance

Refinancing from an FHA loan to a conventional loan is a common method to eliminate MIP. Ensure your home’s current value and your credit profile support this move.

4. Monitor Loan Amortization

Track your loan’s amortization schedule to know exactly when PMI can be canceled.

Table: Conventional vs FHA Mortgage Insurance Removal

| Feature | Conventional Loan (PMI) | FHA Loan (MIP) |

|---|---|---|

| Cancellation Possible | Yes, at 80% equity (request) | Only after 11 years if ≥10% down, otherwise life of loan |

| Automatic Termination | Yes, at 78% equity | No |

| Refinance Option | Yes, to remove PMI | Yes, to remove MIP by converting to conventional loan |

| Payment Method | Monthly | Upfront + Monthly |

Benefits of Removing Mortgage Insurance

Eliminating mortgage insurance is not just about saving money—it also improves your financial flexibility. Benefits include:

- Lower monthly payments – Free up cash for savings, investments, or lifestyle expenses.

- Faster equity growth – More of your payment goes toward principal.

- Enhanced resale value – Buyers appreciate homes without extra insurance costs.

- Better refinancing options – Lower debt-to-income ratios improve loan terms.

Common Mistakes Homeowners Make

Many borrowers remain unaware of when mortgage insurance goes away, which leads to overpaying unnecessarily. Common mistakes include:

- Not requesting PMI cancellation – Waiting for automatic termination can cost months of premiums.

- Ignoring home appreciation – Rising property values can shorten PMI duration.

- Assuming FHA MIP automatically disappears – Only those with ≥10% down and 11-year loans see automatic removal.

- Refinancing too late – Waiting to refinance can result in paying unnecessary MIP.

FAQs About When Mortgage Insurance Goes Away

Q1: Can I remove mortgage insurance before 80% equity?

A1: Typically, no. Most lenders require at least 80% equity for conventional loans, but FHA loans may only allow removal via refinance.

Q2: Does paying extra principal reduce mortgage insurance faster?

A2: Yes. Extra payments increase equity, which accelerates PMI cancellation eligibility.

Q3: How do I calculate when mortgage insurance ends?

A3: Use your loan’s amortization schedule and track your equity growth. For conventional loans, you can request cancellation at 80% equity and automatic removal occurs at 78%.

Q4: Does refinancing always remove mortgage insurance?

A4: Only if you refinance into a loan with 20% or more equity. Refinancing from FHA to conventional is a common method to eliminate MIP.

Q5: Will my mortgage insurance increase if my home value drops?

A5: For conventional loans, PMI premiums are based on loan amount and not home value. FHA MIP is fixed at loan inception.

Conclusion

Understanding when mortgage insurance goes away is critical for smart homeownership. Conventional loans provide clear paths for PMI cancellation at 80–78% equity, while FHA loans require careful planning, especially for small down payments. Homeowners who track their equity, make extra payments, and explore refinancing can save thousands over the life of their mortgage.

By taking proactive steps, you can regain control over your monthly payments, increase equity, and reduce long-term costs—all while staying fully informed about mortgage insurance.